Aveage Read Time: 6–7 minutes.

Yesterday, I treated two patients within the same hour: Maria, a 28-year-old with Type 1 diabetes requiring continuous glucose monitoring and insulin pumps, and James, a healthy 30-year-old in for his annual physical. Both have insurance through the same employer plan and pay identical premiums. How is this possible when Maria’s healthcare costs are easily 50 times higher than James’s?

The answer lies in one of healthcare’s most powerful yet misunderstood concepts: pooled risk. Understanding how risk pooling works isn’t just academic4it directly impacts how we practice medicine, why certain treatments face coverage barriers, and how we can better advocate for our patients within the insurance system.

What Is Risk Pooling? The Mathematical Foundation

Risk pooling is fundamental to the concept of insurance. A health insurance risk pool is a group of individuals whose medical costs are combined to calculate premiums. Think of it as a large pot of money contributed by all plan members.

Here’s the simple mathematics: If 1,000 people each pay $500 monthly into a shared pool, that creates $500,000 per month to cover everyone’s healthcare costs. The healthy members subsidize the costs of those who need extensive care, whilst gaining protection against their own future health risks.

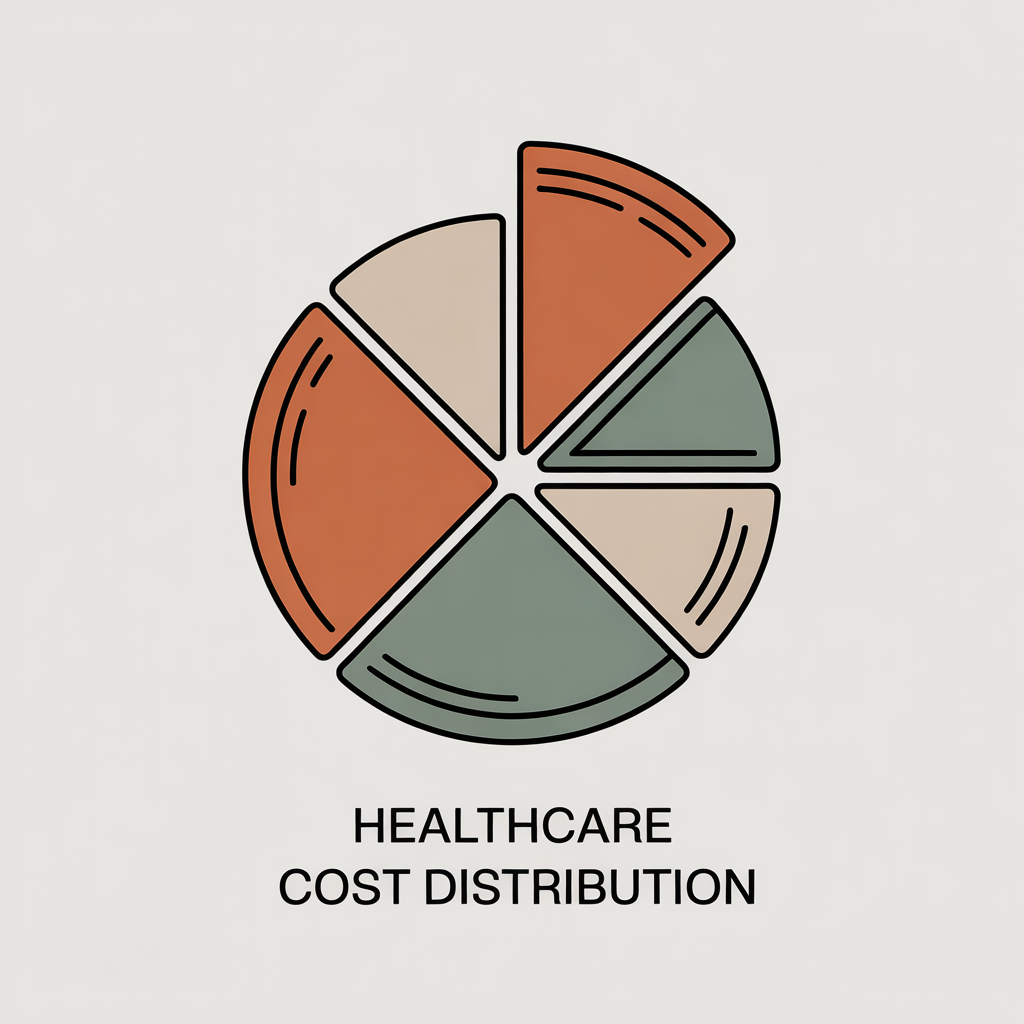

80%

Minimal Healthcare Use

Routine visits, preventive care

15%

Moderate Costs

Chronic conditions, minor procedures

15%

High-Cost Users

Account for 50% of all medical spending

The predictability of these patterns allows insurers to set premiums that keep the system financially stable whilst ensuring comprehensive coverage for all members.

How Pooled Risk Affects Your Daily Practice

Prior Authorisation

Serves as a cost-control mechanism to protect the stability of the risk pool. When we understand this, we can frame our authorisation requests more effectively by demonstrating medical necessity and costeffectiveness.

Coverage Decisions

Based on actuarial data4mathematical analysis of risk and cost. If a plan has an actuarial value of 70%, patients are responsible for 30% of costs on average.

Practical Application for Coverage Advocacy

When advocating for coverage of expensive treatments, frame your request around evidence-based outcomes that justify the cost, prevention of more expensive complications, and comparison to alternative treatments and their costs.

Understanding these mechanisms helps us navigate the system more effectively, transforming frustration into strategic advocacy that benefits our patients whilst maintaining the integrity of the risk pool.

Types of Risk Pools and Their Clinical Implications

Employer-Sponsored Plans

Most stable risk pools with diverse mix of healthy working-age adults. Large group size provides predictable costs and comprehensive benefits. Patients often have more generous benefits and lower out-of-pocket costs.

Individual Market Plans

Can be less stable due to smaller size. Individual market pools may face higher deductibles and more restrictive networks, requiring careful consideration of treatment timing and provider choices.

Medicare and Medicaid

Enormous risk pools providing stability and comprehensive coverage for vulnerable populations. Government programmes represent the largest and most stable pooling mechanisms.

The ACA's Impact: Community Rating

The Affordable Care Act requires insurers to pool all individual market enrollees together, preventing discrimination based on pre-existing conditions and ensuring essential health benefits across all plans.

Working Smarter Within the System

01

Understand Plan Types

Large employer plans offer more predictable coverage with

fewer restrictions, whilst small group and individual plans

may require more prior authorisation documentation.

02

Frame Justifications Strategically

Emphasise cost-effectiveness alongside clinical benefits. Document potential cost savings from preventing complications and reference evidence-based guidelines.

03

Consider Timing and Alternatives

Factor in end-of-year considerations for patients approaching out-of-pocket maximums and step therapy requirements that must be documented.

04

Advocate at Population Level

Support policies that maintain stable, inclusive risk pools and participate in quality improvement initiatives that benefit the entire pool.

Future Considerations

- Value-based care shifting risk from insurers to providers

- Technology integration making risk assessment more precise

- Policy evolution reshaping pooling strategies

Risk pooling isn’t just an abstract insurance concept4it’s the economic foundation that makes comprehensive healthcare coverage possible for our patients. By understanding how it works, we can better navigate coverage decisions, frame our treatment recommendations, and advocate for our patients more effectively.